Let’s be honest, managing money can feel like a constant battle. Between rising costs, subscriptions that sneak up on you, and the ever-present temptation of “just one more thing,”

it’s easy to feel like you’re always playing catch-up. But what if I told you there’s a way to take control? A way to not only manage your money, but to make it work *for* you? This isn’t about deprivation or living a life of restrictions. This is about building a financial plan that gives you freedom and peace of mind. Let’s dive in.

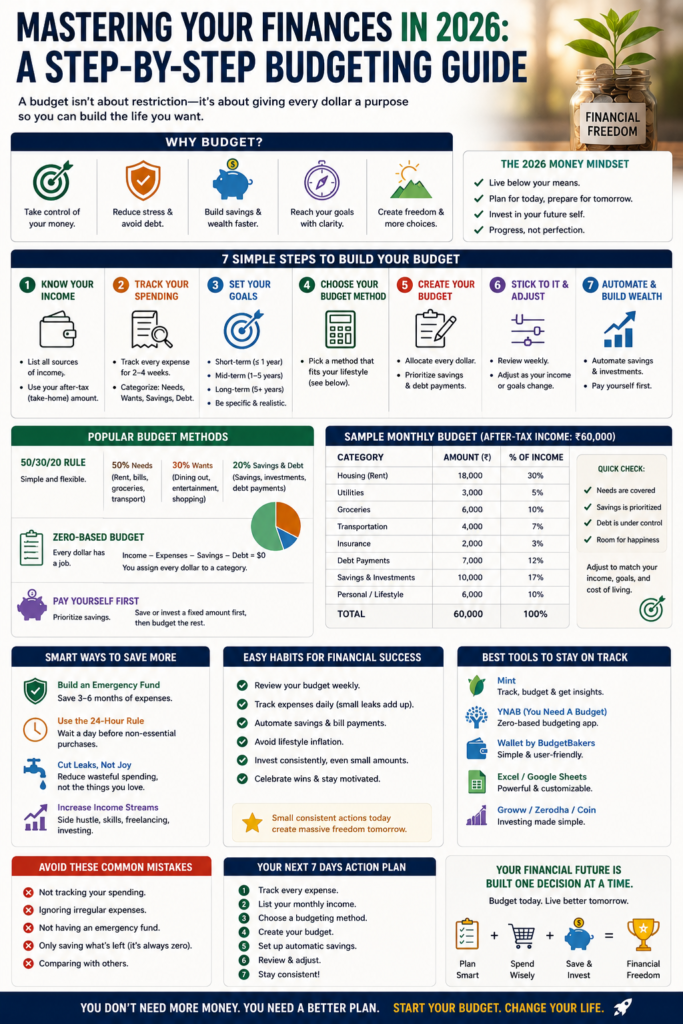

Why Budgeting Matters More Than Ever in 2026

The financial landscape of 2026 is a different beast than it was even a few years ago. Inflation, the rise of digital wallets, and the sheer volume of subscription services we subscribe to

(and often forget about) mean that if you’re not paying attention, your money can disappear faster than you think. A solid budget isn’t just about tracking where your money goes; it’s about building a financial plan. A well-structured budget can help you:

- Manage rising living expenses

- Prepare for emergencies

- Reduce debt efficiently

- Save for both short-term and long-term goals

- Gain peace of mind about your finances

Step-by-Step Guide to Building a Budget That Works

I’ve been helping people get their finances in order for over two decades, and I’ve seen what works and what doesn’t. Forget complicated spreadsheets and rigid rules. The most effective budgets are realistic, flexible, and built for your life. Here’s a proven system:

Step 1: Know Where Your Money Comes From – Calculate Your Income

Before you can do anything, you need to know exactly how much money is coming in each month. This isn’t just about your paycheck (although that’s a big part of it!). You need to account for everything:

- Salary or Wages (after taxes): This is the most obvious one. Use your net income, the amount after taxes and deductions.

- Freelance or Side Hustle Income: Don’t forget any extra income from side gigs or freelance work.

- Investment or Rental Income: If you have investments or rental properties, include the income generated.

- Government Benefits or Stipends: Any government assistance or other regular income should be included.

Mistake to avoid: Using your gross income (before taxes). This gives you an inflated view of what you actually have to spend.

Pro Tip for 2026: If your income varies from month to month, calculate an average over a 3-6 month period to get a more realistic baseline for your budget.

Step 2: Track Every Penny – Monitor Your Expenses

This is the “scary” step for many, but it’s essential. You need to know where your money is going. There are several ways to do this, and the best one is the method you’ll actually stick to. In 2026, there are plenty of options:

- Budgeting Apps: Apps like RelyOwn, You Need a Budget (YNAB), Monarch Money, and PocketGuard can automatically track and categorize your spending. These can be a game changer, especially if you’re new to budgeting.

- Spreadsheets: If you’re a spreadsheet person, create your own or use a pre-made template (plenty are available online).

- Manual Tracking: Yes, you can still use pen and paper! This can be a great way to build awareness of where your money is going.

Mistake to avoid: Only tracking major expenses. Every dollar counts. Even those small coffee runs add up over time.

Pro Tip: Categorize your expenses. Fixed expenses (rent, mortgage, utilities, etc.), variable expenses (groceries, dining out, entertainment), and digital subscriptions are good starting points.

Step 3: Set Clear Financial Goals – Give Your Money a Purpose

Budgeting shouldn’t be about restriction; it should be about empowerment. Setting financial goals gives your budget direction and meaning. Ask yourself: What do you want to achieve?

- Short-term goals: Building an emergency fund, paying off credit card debt, or saving for a vacation.

- Long-term goals: Saving for a down payment on a house, planning for retirement, or funding your children’s education.

Mistake to avoid: Vague goals. “I want to save more” is not as effective as “I want to save $500 by December 2026 for a new laptop”.

Pro Tip: Make your goals SMART (Specific, Measurable, Achievable, Relevant, Time-bound).

Step 4: Choose a Budgeting Method – Find What Fits You

There’s no “one size fits all” when it comes to budgeting. The best method is the one you’ll actually use. Here are a couple of popular options:

- The 50/30/20 Rule: This is a simple starting point. Allocate 50% of your income to needs, 30% to wants, and 20% to savings and debt repayment.

- Zero-Based Budgeting: Every dollar has a purpose. You assign every dollar to a category, so your income minus your expenses equals zero. This can be a more detailed method.

Mistake to avoid: Choosing a method that’s too restrictive or complicated for your lifestyle.

Pro Tip: Don’t be afraid to experiment to find what works best for you.

Step 5: Create Spending Limits – Assign Categories and Stick to Them

Once you’ve chosen a method, you need to assign spending limits to each category. This means deciding how much you can spend on things like housing, transportation, food, entertainment, and savings.

Example Monthly Budget Breakdown: (This is just an example; your numbers will vary)

Housing: 30%

Transportation: 10%

Food: 15%

Savings & Investments: 20%

Personal & Entertainment: 10%

Miscellaneous: 5%

Subscriptions: 5%

Giving: 5%

Mistake to avoid: Setting unrealistic limits. Start with your actual spending patterns (from Step 2) and adjust gradually.

Pro Tip: Use a budgeting app or spreadsheet to track your spending against your limits.

Step 6: Automate Savings and Bills – Make It Effortless

One of the best ways to ensure you stick to your budget is to automate as much as possible.

- Savings: Set up automatic transfers from your checking account to your savings and investment accounts. Pay yourself first!

- Bill Payments: Automate your bill payments to avoid late fees and ensure you’re always up to date.

Mistake to avoid: Relying solely on manual transfers. Life gets busy, and it’s easy to forget.

Pro Tip: Start with a manageable amount for savings and increase it over time as your income allows.

Step 7: Plan for the Unexpected – Build in Flexibility

Life happens. Unexpected expenses will inevitably pop up. That’s why building some flexibility into your budget is crucial.

Here’s how:

- Emergency Fund: Aim to have 3-6 months’ worth of living expenses in an easily accessible savings account.

- “Buffer” Categories: Build extra room into your budget for categories like “miscellaneous” or “fun money” to cover unexpected costs.

Mistake to avoid: Ignoring unexpected expenses altogether. They will happen!

Pro Tip: If an unexpected expense arises, try to find ways to cut back in other areas to stay on track.

Step 8: Review and Adjust Regularly – Stay on Track

Your budget isn’t a “set it and forget it” kind of deal. You should review and adjust it regularly to reflect changes in your income, expenses, and goals.

Here’s how to do it:

- Monthly Review: Track your spending against your budget. Did you stay within your limits? Where did you overspend? Where did you underspend?

- Quarterly Review: Evaluate your progress toward your financial goals. Are you on track to meet your targets?

- Annual Review: Take a broader look at your finances. Are your goals still relevant? Do you need to make any significant changes?

Mistake to avoid: Avoiding the review process. It’s the most important step!

Pro Tip: Don’t be afraid to adjust your budget as needed. Life changes, and so should your financial plan.

Common Mistakes and How to Avoid Them

I’ve seen many people struggle with budgeting, and there are some common pitfalls. Here’s how to avoid them:

- Not Tracking Expenses: You can’t improve what you don’t measure. Make tracking a habit.

- Setting Unrealistic Budgets: Start small and be honest about your spending habits.

- Ignoring Debt: Make a plan to tackle your debt, even if it’s just a small amount each month.

- Giving Up Too Easily: Budgeting takes time and effort. Don’t get discouraged if you slip up.

- Failing to Review and Adjust: Life changes, and so should your budget.

Tips to Improve Your Results and Avoid Future Issues

Want to take your budgeting to the next level? Here are some extra tips:

- Use Technology: Budgeting apps and online tools can simplify the process.

- Seek Professional Help: If you’re struggling, consider working with a financial advisor.

- Educate Yourself: Learn about personal finance. The more you know, the better equipped you’ll be to manage your money.

- Automate, Automate, Automate: Make saving and bill payments automatic.

- Celebrate Your Wins: Acknowledge your progress and reward yourself (within your budget, of course!).

SEO Optimization Tips

In addition to all the practical advice above, it’s worth taking a moment to mention some things that make this guide more visible to search engines like Google. These include:

- Keywords: I’ve woven in keywords such as “budgeting,” “financial planning,” “expenses,” “saving money,” and “2026” organically throughout the text.

- Headings: Clear, descriptive headings (H1, H2, H3) help organize the content and make it easier for readers (and search engines) to understand.

- Readability: The use of short paragraphs, bullet points, and a conversational tone makes the guide easier to read and digest.

Frequently Asked Questions (FAQ)

Start by tracking your income and expenses. Then, set clear financial goals and choose a budgeting method that works for you. Use budgeting apps or spreadsheets to make it easier to track your progress. Regular review and adjustment are key.

The best method depends on your personality and preferences. The 50/30/20 rule is a simple starting point. Zero-based budgeting provides more detailed control.

Popular apps include RelyOwn, YNAB (You Need a Budget), Monarch Money, and PocketGuard. Each app has different features, so try a few to see which one fits your needs.

Aim to save at least 15% of your pre-tax income, including any employer contributions, toward retirement. Even small, consistent contributions build strong habits. The goal is to make savings a “first expense.”

Track your spending to find areas where you can cut back. Consider cooking more meals at home, canceling unused subscriptions, and finding cheaper alternatives for services like insurance and internet.

Make your budget realistic and flexible. Automate savings and bill payments. Review your budget monthly and adjust as needed. Set clear, measurable goals.

Look for opportunities to increase your income, such as a side hustle or part-time job. Identify areas to reduce expenses, such as negotiating lower insurance rates or canceling unused subscriptions.

Budgeting may seem daunting, but it’s one of the most powerful things you can do to take control of your financial life. By following these steps and adapting them to your unique situation, you can build a budget that helps you achieve your goals and live a more secure and fulfilling life in 2026 and beyond. Take action today. You’ve got this!